A 1035 exchange is the process of selling one insurance contract and replacing it with another in a “like kind exchange” and realizing specific tax advantages.

A life insurance policy can be sold and the proceeds used to purchase another life insurance policy, a non-qualified...

Read full article »

When you apply for a life insurance or annuity product utilizing a 1035 exchange, you can expect the following steps to occur:

1. Application: During this step, you will sign documents authorizing an insurance company to become the holder of your non-tax qualified funds. You...

Read full article »

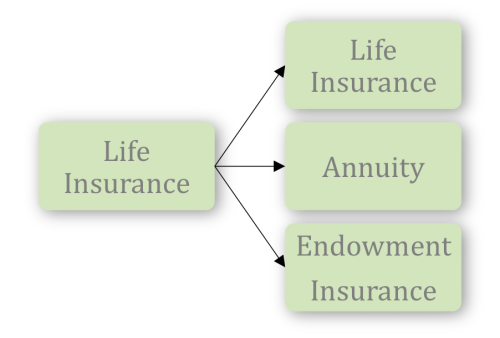

A Life insurance policy can be exchanged for another life insurance policy, an endowment insurance policy or a non-qualified annuity.

Read full article »

Read full article »

The main purpose of a 1035 exchange is to avoid the tax implications of selling a life insurance policy, an endowment, or an annuity. By taking advantage of the US Tax code that allows you to exchange certain items for other like items you can...

Read full article »

§ 1035. Certain exchanges of insurance policies

(a) General rules

No gain or loss shall be recognized on the exchange of—

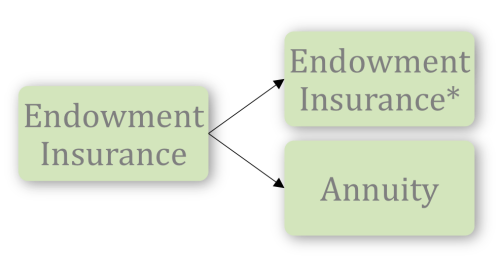

(1) a contract of life insurance for another contract of life insurance or for an endowment or annuity contract; or (2) a...

Read full article »

§ 1031. Exchange of property held for productive use or investment

(a) Nonrecognition of gain or loss from exchanges solely in kind

(1) In general No gain or loss shall be recognized on the exchange of property held for productive use in a...

Read full article »